Alibaba: Most Own-able Business

Alibaba: Most Own-able Business

A great business worth looking at

Peter Lynch, the great fund manager once said (I am paraphrasing here, of course!) that big companies make small moves whereas small companies tend to make bad moves. Understandable, yes. But here is something to ponder on:

I think the changing landscape with influx of technological changes makes this advice obsolete. I think if large companies, under their heavy veil, still try to do the heavy lifting and take ‘calculated’ and ‘bold’ (not necessarily an oxymoron) moves, large companies can make large moves!

I invest a lot of my capital in large stock companies- mainly in Indian and US capital markets. I am a young person relatively that can take risks but still tend to deploy my capital in large companies because I try to identify ‘large companies making bold moves’.

You want examples? Some of my favorites include Amazon, Intel, Nvidia, Apple and what will be the main subject of this newsletter- Alibaba!

Short History

Alibaba started in 1997 by Jack Ma and close to 20 of the other co-founders. The company was started with $80,000 by raising it from close to 80 other investors. The company had its humble beginnings as an online bulletin board of local businesses.

Let’s talk about this man for a second. He was born in 1964, not academically bright. He unlike general Silicon Valley was not a ‘computer guy’. He wasn’t good at math. Also, widely reported, he couldn’t get a job even at McDonald’s!

But, as history goes, successful people have generally grabbed opportunities in their surroundings and make it big.

Bill Gates- software theme, Steve Jobs- personal computer, Elon Musk- digital payments-electric vehicles etc. Ma took the opportunity of increasing incoming of tourists to China and learned English. He started working as a tourist guide and later as an English teacher at a school.

During 1990s, entrepreneurship wasn’t looked as a bright career prospect. Ma started his first venture- China’s Yellow Pages which later he had to give up.

Business Overview

If you don’t know this, Alibaba Group is not only an e-commerce company. It is a cloud computing, digital media, entertainment and a financial company. The company has focused on creating platforms or in better words ecosystems in play around their core businesses.

Their e-commerce is not only a B2C operation but also includes B2B operations, also including cross export-import operation through a subsidiary. The company generates revenue from merchants through the sale of a variety of marketing services, membership fees, customer management services, product sales, commissions on transactions, and software service fees.

The company also has a whole sale business operation, providing same monetisation opportunities as retail. Alongside, the usual services they also provide data analytics, store front management tools etc. They charge set up and subscription fees from the merchants.

The company has focused on digitalization of its offerings. An example: un-like Amazon, they were finding it difficult to provide last mile delivery services in China which consist of extensive congested rural areas and not so planned infrastructure for some of the far flung areas. The logistic companies which they partnered with initially couldn’t provide these services due to which some of the e-commerce competitors including Amazon and e-Bay could have taken the inroads. Solution? They like Amazon invested in operational research and supply chain management to build their expertise in last mile connectivity.

Alibaba’s cloud computing offering is third largest in the world in revenue terms. Largest in China, providing computing services include elastic computing, database, storage, network visualisation, large scale computing, security, management and application, big data analytics, a machine learning platform and IoT devices.

Alibaba has a focus on capturing the full value chain of a consumer. They believe that digital entertainment is the natural extension of their core e-commerce offering. Their streaming service is the third largest in China in terms of MAU. They also own Alibaba Pictures, providing content production, promotion, distribution, IP licensing and integrated management, and online cinema ticketing. Here, they used data from their core e-commerce operation to showcase relevant content to the consumer (through data harvesting and proprietary data science algorithms.

They are also into mobile video gaming through Lingxi Games.

They have also kept a core focus on monetization of their platforms. Alimama- an AI driven monetization platform that helps match marketing demands of merchants, brands and retailers on their platform. This platform supports P4P marketing services that are based on keyword search rankings, in feed marketing services, data derived from e-commerce app etc.

Alimama works exactly like Google Adwords. They provide affiliate marketing services to third party companies and any company per se which wants to display adds.

Net net basis- they understand Professor’s Damodaran’s new age company valuation methodology. It states that for a platform to derive better valuation- the platform should be engaging and the users should spend huge amounts of time for the company to have upsell and downsell opportunities.

In my view, Alibaba has interesting growth opportunities going forward. They are still in the nascent stage of monetising their offerings and what excites me is their ‘innovative’ section under their business overview section of the annual report.

They also own 33% of Ant Financial- a financial services platform which is arguable the most important subsidiary company of the group. It started with Alipay in 2000s to act as an escrow payment platform like the way Paypal works for e-Bay.

Ant Financial has the largest money market product even bigger than JP Morgan! It helps manage Chinese financial lives. It helps in wealth management, insurance, investment, payment processing etc.

Ant Financial has the possibility of becoming larger than Alibaba Groups as a whole!

The company is also working on a new retail strategy which is on ‘developing stage’

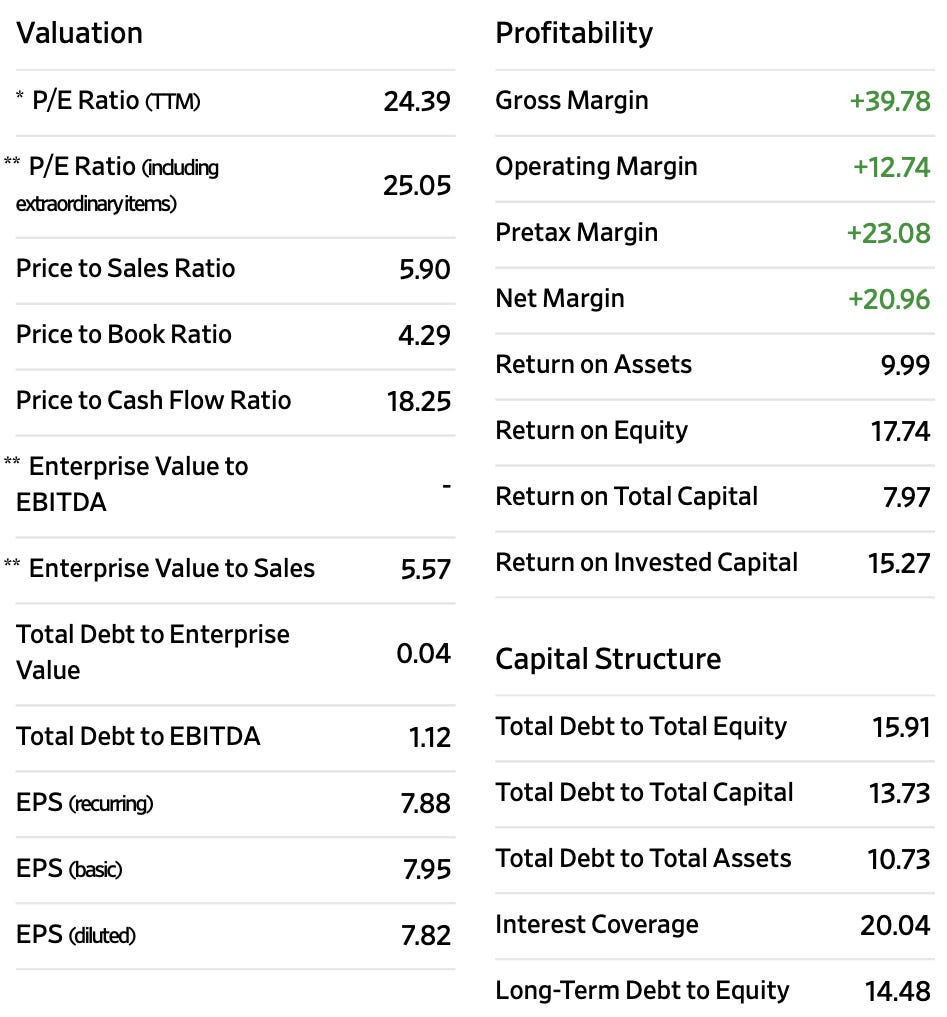

Financials

Accounting is the language of the business. Let’s see how the historical financials look like

Source: Statista 2021 The company has been able to compound its revenue by 50.66% over the past 10 years! So much for small moves for a large company!

The company has been consistently earnings its revenue majorly from its e-commerce operation.

Source: Annual Report FY21

Major risk include concentration of revenue- arising from their core operation.

Apart from their e-commerce operation and financial platform, no other business division is performing at par. This is a major risk- as the business has to reinvest in these business segments to increase the revenue and their respective EBITDAs.

The company has been funding the other businesses from their core business i.e. the main cash generation machine.

Main insight: Other businesses apart from e-commerce, has been in the growth stage and requires Capex to fund the losses. All these businesses are future driven and requires intensive monetisation efforts with acute execution.

This has to be observed going forward.

In my view, the financials look quite promising and the company is bound to grow atleast by a conservative basis 30-35% going forward. If we take an assumption that the smaller business segments start being EBITDA+ in the next 5 years- the p/e can be re-rated to 30+ easily with higher growth- 40%+

These numbers may look too optimistic. But they seem realistic if we look closely at the above mentioned qualitative and quantitative figures.

The company has been able to increase its operating cash flow by 23.4% CAGR. The company has also converted 32% of its sales into cash which is again a solid performance when the net profitability of the company has been in 20%+ range!

The company has also been decreasing its % proportion of sale on Capex- a positive for the loss making business units to start firing on different fronts. An assumption of 5 years hence is a conservative base to support the above given thesis.

Myth1: Amazon’s Alter Ego?

Lot of investors and general populace believe that Alibaba like other Chinese companies have copied the ‘tech’ or ‘IP’ from their Western (American majorly) counterparts. Look deeper and you will find some major differences.

Amazon did its IPO in 1998 when it was ONLY an online book seller on an ‘obscure’ concept called the internet. Alibaba was started as a reseller of goods produced by local businesses-being a pioneer of current concepts ‘platformisation’ and ‘ online marketplaces’

Alibaba didn’t start as an internet company unlike Amazon. The former was initially like ‘yellow pages’ popular in the US.

One important facet where both of these behemoths are widely different is that the former has focused on owning their warehouses and logistics. Alibaba never focused on owning their logistics. They focused on investing in logistic and warehouses companies. Alibaba has focused on keeping its model as asset light as possible!

Myth2: Amazon is bigger

Amazon is smaller vis-à-vis Alibaba. I hear you wonder- what the heck am I talking about?

Let’s see the difference between the GMV (Gross Merchandise Value- the amount of transaction value) between these two companies.

Amazon’s GMV (including third party sellers and own products): $475 B

Alibaba’s GMV: $1.2 T

Alibaba’s GMV doubled y-o-y from the last year. Now, this can be a one off event from the Pandemic but an amazing achievement for a large company! And against, the common ‘wisdom’ of large companies not able to make major moves

Alibaba has a scale which Amazon has not able to achieve. This is in sharp contrast to the common notion of Amazon being a global player where Alibaba being a puny player relatively.

Alibaba has a 25% share in total retail spending in China. Alibaba achieved 1B active global users (recorded till March 2021) ~ i.e., 3X the population of USA! These 1B users bought something off Amazon twice each week!

Huge headroom to grow more!

Recent DEBACLE

Chinese government has heavily clamped down on their tech companies including Alibaba with recently imposed $2.8B fine!

This is a huge socio-political ‘noise’ that is giving a SALE opportunity for buying this wonderful future driven business.

However, it is surely a cause of worry for investors.

Better strategy- focus on business fundamentals and try to look at the broader situation more objectively. If you have read about Chinese socio-political history, you will realise that Chinese works on one goal- to be on the top and be the best. They recognise one important dimension which I believe western and general populace don’t that there is a difference between consumer electronic companies which are customer driven and make us consume better but they are not ‘tech’ companies as we all generally call them.

Tech companies are companies that are engaged in some research activities not for the ‘goods’ or ‘consumer app/software’ but like technological medical devices/defence/biotech etc.

Chinese are inherently communists and they recognise the above and hence wants to take back the power from their consumer electronic or e-commerce companies, which can create short term pains (for these companies and consumers) but these businesses will recognise and adapt by being more balanced as far as their geographic revenue distribution goes which can hedge the concentration issue- which Alibaba faces (80% of revenue from China)

Disclosure: I own Alibaba shares in my portfolio. Views are biased and this is just for research and information purposes. Not to be taken as an investment advice.